Unlock a HELOC: Discover the Buying Power in your Home

When my husband and I decided to get married, we began searching for our perfect home. We found it quickly – too quickly. In order to buy it, I still needed to make some updates to sell the house I was already living in. Yikes, I thought, how do people juggle these kinds of situations that require cash invested in a home? My mortgage lender had the answer: take out a HELOC.

A what??

What is a HELOC?

A HELOC, I quickly discovered, is a Home Equity Line of Credit. I had a line of credit based on the value of my home that I knew nothing about.

The HELOC was my security blanket. It allowed me to use the equity in my house to get the money I needed to make sure my husband and I didn’t miss out on our forever home.

HELOCs aren’t just for new home buying. The funds may be used for a variety of needs, including home improvements, debt consolidation, education, or to pay for a big event like a wedding. The funds from a HELOC can also give you more cash bargaining power if you’re purchasing a big-ticket item like a car, boat, or RV.

When it comes to these types of needs, think of your house as a credit card. Instead of getting a lump-sum loan, a HELOC enables you to draw funds to pay for the things you need, then pay down the loan.

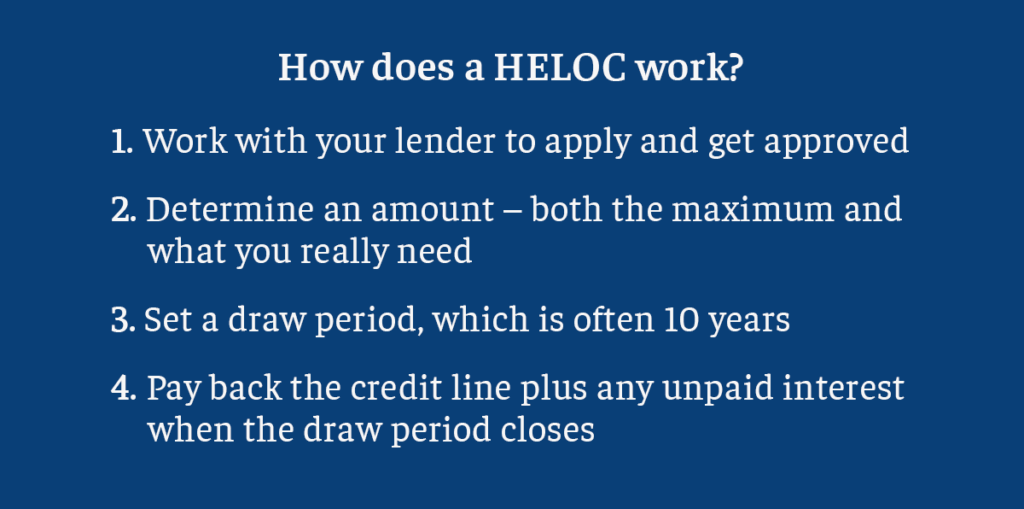

How does a Home Equity Line of Credit work?

- Work with your lender: Each lender sets the requirements for obtaining a HELOC. These are usually the typical things lenders look at when a customer applies for a loan. That includes the equity in the house, loan-to-value and debt-to-value ratios, and the borrower’s credit score.

- Determine an amount: The borrower determines how much money to take out or draw from a HELOC. The borrowing cap for most lenders is 80% of the home value. The total HELOC amount may exceed the amount that is drawn, meaning you don’t have to take out the maximum amount you’re approved for. For example, you may be approved for a $50,000 HELOC, but only need to draw $20,000.

- Set a draw period: The draw period is the span in which the borrower may access HELOC funds, often 10 years. Because it’s an open-end line of credit, the borrower does not have to draw funds until needed. He or she can draw from the HELOC any time within that period. If the principal balance is paid back within the draw period, the funds can be accessed for additional rounds.

- Pay back the credit line: When the draw period ends, the borrower must repay the amount that was actually drawn on the HELOC.

- During the draw period, the borrower will make minimum monthly payments, typically interest on the amount borrowed.

- At the end of the draw period, the HELOC closes and the balance of the amount drawn plus any unpaid interest needs to be repaid.

- Work with your loan officer to discuss the variety of options for repayment.

Using a HELOC for a new home purchase, I was able to pay back and close the line of credit after the sale of my old house, reducing the draw period. Every situation is different. But one thing is true for all: It’s important to work with a trusted loan officer, like those on our team at Union Savings Bank, who can guide you through the process and put you on the path that’s right for you.