Starting the journey to homeownership is an exciting endeavor, but the obstacle of saving for a down payment can feel strenuous. We review top tips that offer practical strategies to help you accumulate the funds needed for a down payment. From covering budgeting to exploring alternative income streams, join us as we present the secrets to saving efficiently, bringing you one step closer to unlocking the door to your future home.

1. Create a Budget

Start your budget by listing all income sources and categorizing essential expenses, such as rent or mortgage, utilities, and groceries. Next, evaluate your monthly expenses and identify areas where you can make cuts, including canceling subscription services, dining out less, or finding more cost-effective alternatives for regular expenses. Finally, regularly track and review your budget, adjusting as needed to stay on course and ensure steady progress toward accumulating the necessary funds for your dream home.

2. Set a Realistic Goal

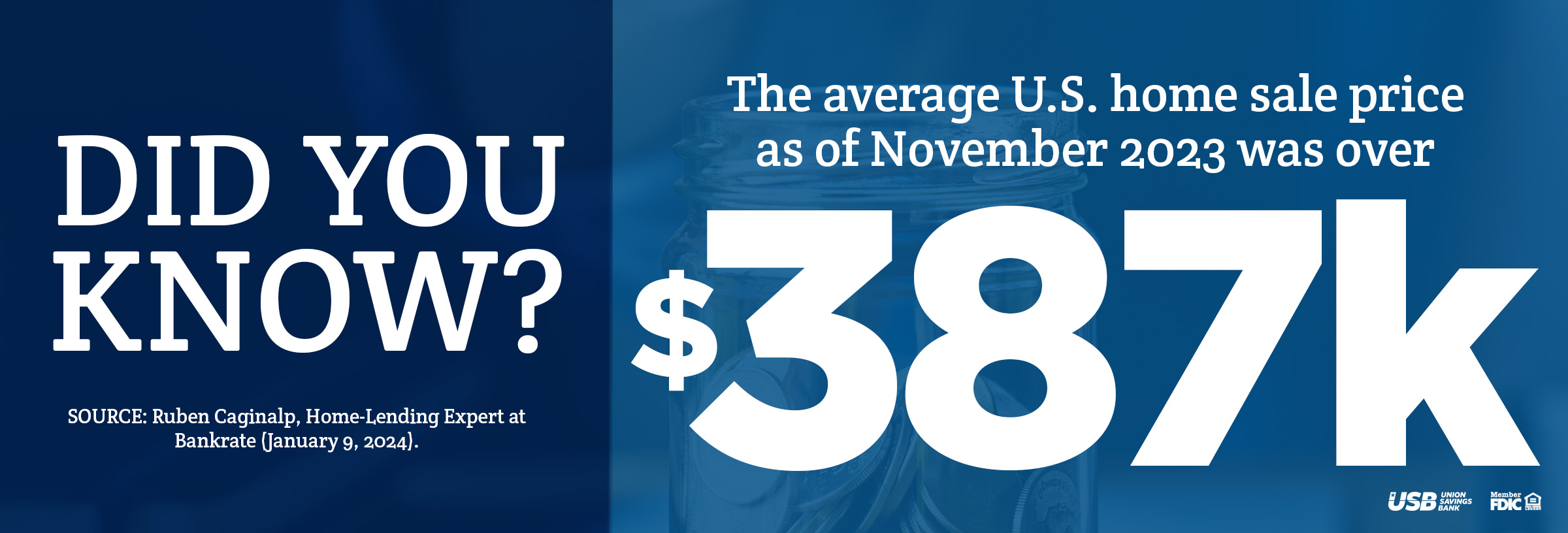

You can determine the amount you need for a down payment based on the cost of homes in your desired location while also setting a clear timeframe. This will help you stay focused and motivated throughout the saving process. A well-defined goal can help you establish a feasible savings plan, preventing frustration or burnout that may arise from setting unattainable objectives. Realistic goals also can enable you to track your progress, celebrate milestones, and stay motivated throughout the saving process.

3. Automate Your Savings

Setting up automatic transfers to your dedicated down payment savings account can ensure that a portion of your income goes directly toward your monthly goals, making it easier to stay consistent with your savings efforts. This streamlines the process and helps you steadily accumulate funds without the need for constant manual transfers, promoting a less stressful and effective savings strategy.

4. Explore Down Payment Assistance Programs

Leveraging government or local assistance programs may expedite the path to homeownership, especially for those with limited savings. Additionally, these programs can offer favorable terms, lower interest rates, or forgivable loans, further easing the financial burden associated with acquiring a property and making homeownership more accessible. A typical down payment percentage is 3.5%–20% of the expected purchase price plus the closing costs and potential escrow funding. Contact a USB loan officer at (833) 301-2505 to learn more about the down payment assistance programs we have to offer and see what your potential loan could look like.

5. Consider a High-Interest Savings Account

Every bit of interest earned can contribute to your down payment fund over time. Increased interest earnings may accelerate the growth of your down payment fund, helping you reach your homeownership goal faster. Furthermore, high-interest savings accounts typically provide a safe and liquid investment option, allowing you to preserve your capital while maintaining accessibility to your funds when needed for a home purchase. At Union Savings Bank, we offer a Maximizer Savings Account with competitive interest rates. Stop by, call your local branch, or visit our website to get more information about opening an account.

6. Avoid New Debt

Avoiding new debt while saving for a down payment can be crucial because high-interest loans or credit card debt may strain financial resources, diverting money away from your savings goal. Eliminating existing debt can free up more disposable income to channel into your down payment fund and speed up accumulating sufficient funds. Additionally, a lower debt-to-income ratio may enhance your financial standing, making it easier to qualify for a mortgage and secure better loan terms when the time comes to purchase a home.

7. Regularly Review Your Budget and Savings Progress

If you encounter challenges or changes in your financial situation, you may adjust your savings plan accordingly. Consistent monitoring ensures you stay on track and make necessary adjustments. This proactive approach may help you identify potential areas for additional savings, making it easier to allocate more funds toward your down payment. Furthermore, consistent budget reviews can provide a sense of accountability and motivation, helping you stay on track and maintain the discipline needed to achieve your homeownership aspirations.

Saving for a down payment is a significant financial milestone on the path to homeownership. Employing strategic methods can make this journey more manageable. These tips may offer a comprehensive guide to building the financial foundation needed to purchase a home. By incorporating these practices into your financial routine, you can pave the way to homeownership and cultivate a sustainable approach to managing your finances. Every small step today brings you closer to the keys to your future home tomorrow.

All home-lending products are subject to credit and property approval. Rates and program terms and conditions are subject to change without notice. Other restrictions and limitations apply.

These articles are for educational purposes only and provide general mortgage information. Products, services, processes, and lending criteria described in these articles may differ from those available through Union Savings Bank. For more information on available products and services and to discuss your options, please contact a Union Savings Bank loan officer.

NMLS# 446047