Certificate of Deposit vs. Maximizer Savings Account: What’s the Difference?

Certificate of deposit. Maximizer savings account. Banking terms like these might sound like a different language if you’ve never learned them before. Today, we’ll dive into the world of savings to help you understand key phrases.

What’s a certificate of deposit (CD)?

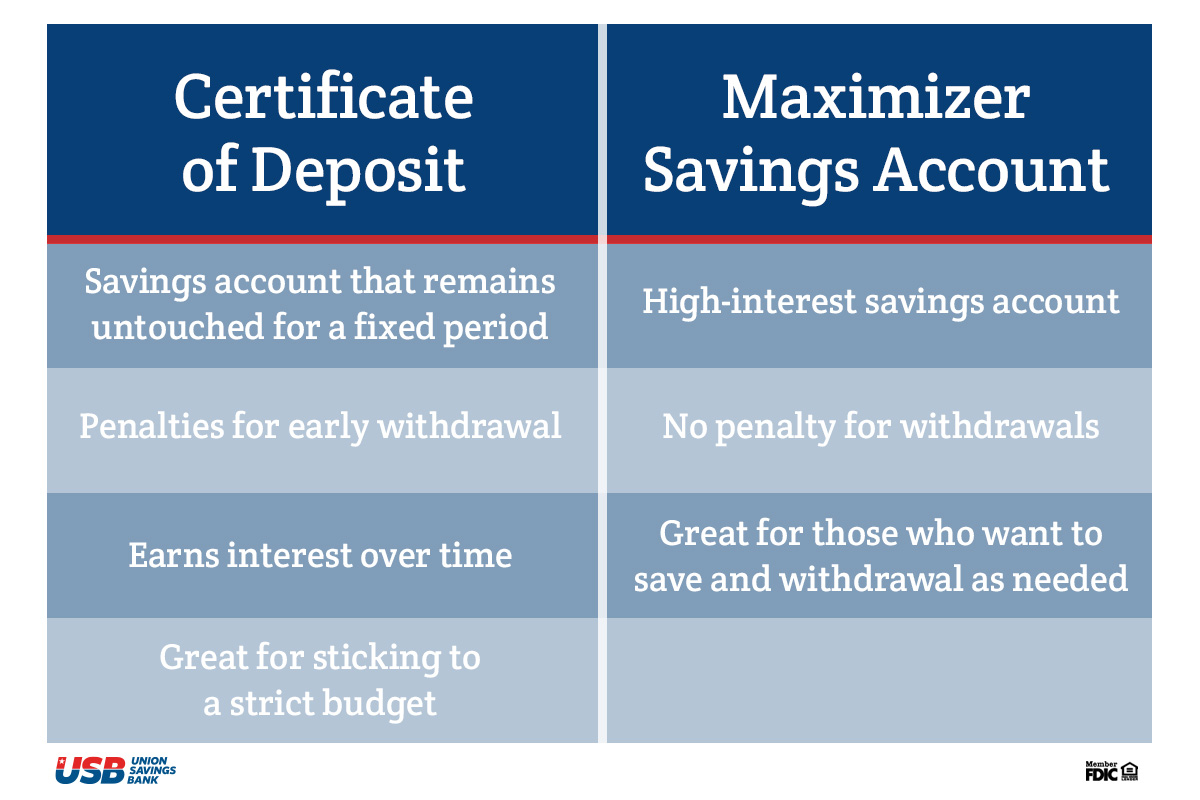

A certificate of deposit (CD) is a savings product that earns interest on a lump sum or fixed amount for a fixed period. CDs differ from savings accounts in that the money must remain untouched for the entirety of the term or risk penalty fees or lost interest. CDs usually have higher interest rates than other savings accounts as an incentive for lost liquidity (the ability to deposit and withdraw money).

What’s a maximizer savings account?

This type of savings account is a high-interest liquid account that allows you to put money into and take money out of your account with no penalty. The interest rate is not fixed, which means that it goes up or down based on factors such as inflation, competition between banks, and changes to the Federal Reserve’s benchmark interest rate. It’s like a regular savings account but with a higher interest rate.

Why choose a CD or a maximizer savings account?

There are many benefits to opening a CD and/or a maximizer savings account. Because a CD account can penalize you for withdrawing early, it’s a great way to avoid being tempted to spend your savings. You’ll also earn additional money (interest), which “rewards” you for leaving your account alone.

Of course, financial emergencies can happen. If you think you might need that rainy day fund, a maximizer savings account presents an opportunity to earn a high-interest amount without the high penalties if you need to withdraw early.

When John Dunn, USB’s VP Branch Coordinator, was asked what one piece of advice he’d give to people wanting to build a foundation for financial success, he said, “Pay yourself first. Invest in your future as early and with as much as possible. Bills will always be there, but your future deserves attention too. The compounding dollars will make the early pain worth it over time. The size of investment is secondary to starting your savings.”

We understand that this is a lot of information. Save this chart for a quick refresher:

It’s never a bad time to start saving! Union Savings bank offers highly competitive savings rates for CDs and maximizer savings accounts. Start paying yourself first today; call or visit your local USB branch to find our current savings rates!

NMLS# 446047